Best of Municipal Market - August 2014

•

1 recomendación•966 vistas

Best of Municipal Market - August 2014

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (19)

Destacado

Destacado (20)

Similar a Best of Municipal Market - August 2014

Similar a Best of Municipal Market - August 2014 (20)

Más de Bloomberg Briefs

Más de Bloomberg Briefs (20)

Último

Último (20)

Best of Municipal Market - August 2014

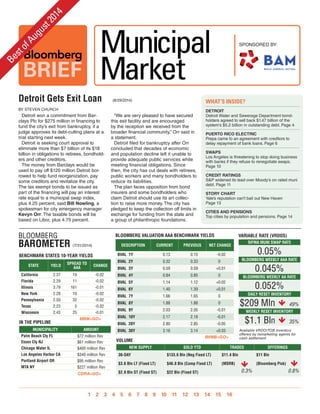

- 1. Detroit Gets Exit Loan (8/29/2014) Detroit won a commitment from Bar-clays Plc for $275 million in financing to fund the city’s exit from bankruptcy, if a judge approves its debt-cutting plans at a trial starting next week. Detroit is seeking court approval to eliminate more than $7 billion of its $18 billion in obligations to retirees, bondhold-ers and other creditors. The money from Barclays would be used to pay off $120 million Detroit bor-rowed to help fund reorganization, pay some creditors and revitalize the city. The tax exempt bonds to be issued as part of the financing will pay an interest rate equal to a municipal swap index, plus 4.25 percent, said Bill Nowling, a spokesman for city emergency manager Kevyn Orr. The taxable bonds will be based on Libor, plus 4.75 percent. “We are very pleased to have secured this exit facility and are encouraged by the reception we received from the broader financial community,’’ Orr said in a statement. Detroit filed for bankruptcy after Orr concluded that decades of economic and population decline left it unable to provide adequate public services while meeting financial obligations. Since then, the city has cut deals with retirees, public workers and many bondholders to reduce its liabilities. The plan faces opposition from bond insurers and some bondholders who claim Detroit should use its art collec-tion to raise more money. The city has pledged to keep the collection off limits in exchange for funding from the state and a group of philanthropic foundations. BY STEVEN CHURCH WHAT’S INSIDE? DETROIT Detroit Water and Sewerage Department bond-holders agreed to sell back $1.47 billion of the system’s $5.2 billion in outstanding debt. Page 4 PUERTO RICO ELECTRIC Prepa came to an agreement with creditors to delay repayment of bank loans. Page 6 SWAPS Los Angeles is threatening to stop doing business with banks if they refuse to renegotiate swaps. Page 10 CREDIT RATINGS S&P widened its lead over Moody’s on rated muni debt. Page 11 STORY CHART Yale’s reputation can’t bail out New Haven Page 13 CITIES AND PENSIONS Top cities by population and pensions. Page 14 BLOOMBERG VALUATION AAA BENCHMARK YIELDS DESCRIPTION CURRENT PREVIOUS NET CHANGE BVAL 1Y 0.13 0.15 -0.02 BVAL 2Y 0.32 0.33 0 BVAL 3Y 0.59 0.59 +0.01 BVAL 4Y 0.84 0.85 0 BVAL 5Y 1.14 1.12 +0.02 BVAL 6Y 1.40 1.39 +0.01 BVAL 7Y 1.66 1.65 0 BVAL 8Y 1.88 1.88 0 BVAL 9Y 2.03 2.05 -0.01 BVAL 10Y 2.17 2.18 -0.01 BVAL 20Y 2.80 2.85 -0.05 BVAL 30Y 3.16 3.14 +0.03 BLOOMBERG BAROMETER (7/31/2014) BENCHMARK STATES 10-YEAR YIELDS STATE YIELD SPREAD TO AAA CHANGE California 2.37 19 -0.02 Florida 2.29 11 -0.02 Illinois 3.79 161 -0.01 New York 2.28 10 -0.02 Pennsylvania 2.50 32 -0.02 Texas 2.23 5 -0.02 Wisconsin 2.43 25 -0.01 VOLUME NEW SUPPLY SOLD YTD TRADED OFFERINGS 30-DAY $133.6 Bln (Neg Fixed LT) $11.4 Bln $11 Bln $3.6 Bln LT (Fixed LT) $46.8 Bln (Comp Fixed LT) (MSRB) (Bloomberg Pick) $2.9 Bln ST (Fixed ST) $22 Bln (Fixed ST) 0.3% 0.8% IN THE PIPELINE MUNICIPALITY AMOUNT Palm Beach Cty FL $72 million Rev Essex Cty NJ $61 million Rev Chicago Water IL $400 million Rev Los Angeles Harbor CA $340 million Rev Portland Airport OR $95 million Rev MTA NY $227 million Rev VARIABLE RATE (VRDOS) SIFMA MUNI SWAP RATE 0.05% BLOOMBERG WEEKLY AAA RATE 0.045% BLOOMBERG WEEKLY AA RATE 0.052% DAILY RESET INVENTORY $209 Mln 49% WEEKLY RESET INVENTORY $1.1 Bln 35% Available VRDO/TOB inventory offered by remarketing agents for BVMB<GO> cash settlement MBM<GO> CDRA<GO> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 BRIEF Municipal Market Best of August 2014 SPONSORED BY:

- 2. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 2 DIARY BRIAN CHAPPATTA (8/29/2014) Pennsylvania Turnpike Bonds With Negative 88 Percent Yield Show Risk of Ignoring Calls Investors holding some escrowed-to-ma-turity Bloomberg Brief Municipal Market Bloomberg Brief Ted Merz Executive Editor tmerz@bloomberg.net +1-212-617-2309 Bloomberg Brief Jennifer Rossa Managing Editor jrossa@bloomberg.net +1-212-617-8074 Municipal Market Joe Mysak Editor jmysakjr@bloomberg.net 212-617-2323 Editor Taylor Riggs triggs2@bloomberg.net 212-617-2072 Reporter Brian Chappatta bchappatta1@bloomberg.net 212-617-0698 Contributing Sowjana Sivaloganathan, Analysts Bert Louis Newsletter Nick Ferris Business Manager nferris2@bloomberg.net 212-617-6975 Advertising Adrienne Bills abills1@bloomberg.net 212-617-6073 Reprints & Lori Husted Permissions lori.husted@theygsgroup.com 717-505-9701 x2204 To subscribe via the Bloomberg Terminal type BRIEF <GO> or on the web at www.bloombergbriefs.com. To contact the editors: munimarket@bloomberg.net This newsletter and its contents may not be forwarded or redistributed without the prior consent of Bloomberg. Please contact our reprints and permissions group listed above for more information © 2014 Bloomberg LP. All rights reserved. bonds from the Pennsylvania Turn-pike Commission will have the debt called back next month at par, in a blow to buyers who purchased the securities at significant premiums as recently as last week. Turnpike bonds issued in 1998 that ma-ture in December 2027 traded Aug. 13 at 107 cents on the dollar, the highest price since January, data compiled by Bloom-berg show. With the issuer reserving the right to exercise par call provisions, the price was equivalent to a negative 88 percent yield-to-worst. The worst became a reality on Aug. 18, when a notice was filed that the almost $73 million of debt would be called on Sept. 17 at a redemption price of 100 cents on the dollar. Bonds that mature from 2014 to 2018 and a $42 million series due in 2023 will also be called at par. Prices plunged to 99.8 cents. The Pennsylvania Turnpike debt had com-manded premium prices long before muni yields fell to near the lowest in a generation. After the bonds were advance refunded in 2003, with state and local government secu-rities, or SLGS, deposited in escrow as col-lateral, prices have often jumped above 100 cents even with the call provision looming. Bonds that are escrowed to maturity pay principal and interest payments through an account that maintains the funds need-ed to meet future obligations. Muni issuers use SLGS or U.S. government securities as collateral, making the debt attractive to investors because the probability of repay-ment no longer rests with the fortunes of the state or municipality. Yet the name can be misleading, as some investors found out in the 1980s. The Kansas City Board of Public Utilities had planned to call some bonds that were escrowed-to-maturity in 1994 instead of from 1997 through 2001 after its bond coun-sel said call options remained intact. The bond issue was eventually canceled after bond counsel failed to deliver documents. Still, confusion ensued among issuers and regulators, and investors grew frustrat-ed at the depressed prices on escrowed-to- maturity securities. What resulted was a move towards better information that eventually became the MSRB’s Electronic Municipal Market Access website. The Pennsylvania Turnpike’s bond call shows that even with the bolstered transparency, investors may still be caught unaware. On the CUSIP’s DES page on the Bloomberg Terminal, the refunding information section indicates that although the debt is escrowed to maturity, call pro-visions may be exercised. SUPPLY AND DEMAND (8/29/2014) Inflows Overpower Supply Increase, Yields Decline 50 40 30 20 10 0 Monthly Flows Monthly Supply Average 10-Year Yield The weekly-average municipal bond yield in August fell to its lowest since May 2013 to 2.23 percent, even as debt sales rose to $29.6 billion in the month. Demand, as measured by inflows into Lipper US Fund Flows, was the highest since May after investors poured $1.56 billion in cash into muni bond funds in August. Funds that 3.5% 3.0% 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% report weekly to Lipper reported $446.4 million in inflows for the week ended Aug. 27. Long-term funds recorded $288.4 million of inflows while high-yield funds had $229.8 million of inflows. Intermediate funds that report weekly saw $137.7 million of inflows, the only category to see an increase week over week. -10 Aug 2013 Sep Oct Nov Dec Jan 2014 Feb Mar Apr May Jun Jul Aug $ In Billions Source: Bloomberg — Taylor Riggs 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 3. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 3 LOW-RISK, MUNICIPAL-ONLY UNDERWRITING WAS ALL PART OF THE PLAN. Bond insurance isn’t a commodity anymore — Build America Mutual’s unique characteristics set us apart. Visit buildamerica.com/mission to learn what else makes us diff erent, including: • BAM’s mutual structure, which means a stronger balance sheet and durable ratings • Obligor Disclosure Briefs — free, annual updates on every credit we insure • “First-loss” reinsurance that protects BAM’s capital from claims • Unique economic benefi ts for issuers © 2014 Build America Mutual sponsored by 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 4. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 4 NEWS California Boosts Hollywood Credit (8/28/2014) California Governor Jerry Brown and lawmakers struck a deal to more than triple the tax credit for Hollywood studios to stem the flight of film and TV production to other states. The $330 million annual subsidy, announced yesterday by the governor’s office, is second only to New York’s $420 million in tax breaks for productions and outpaces incentives by Louisiana, Georgia and Florida, according to state analysts. More than 40 projects sought and failed to win some of the $100 million California allocated for production subsidies last year, when $1.06 billion worth of work went outside the state, according to the California Film Commission, which administers the program. The agreement “once again makes California a viable place to film the big-budget movies and TV shows that generate thousands of jobs and millions in revenue and spending,’’ Chris Dodd, chair-man and chief executive officer of the Motion Picture Association of America, said yesterday in a statement. “It stands to bring billions of dollars into the California economy.’’ California’s tax incentives to film and television studios began in 2009 and have helped keep as many as 51,000 jobs from leaving the state, according to a statement from state Assemblymen Raul Bocanegra and Mike Gatto, both Los Angeles-area Democrats who sponsored the original bill. The deal eliminates a budget cap that excluded big-budget films from applying for the credits and makes them available to more TV shows as well, Gatto said. “We’re trying to seek productions that employ the most Cali-fornians for the longest duration,’’ he said in an interview. The mayors of California’s largest cities lobbied lawmakers earlier this month for a $400 million incentive package. It was reduced to $330 million after discussions with Brown. “The heart and soul of the entertainment industry are the artisans, craftspeople and tradespeople who you never see on screen, and that’s who will benefit from this legislation,’’ Los Angeles Mayor Eric Garcetti said in a statement. “We are the entertainment capital of the world and this legislation will make sure it stays that way.’’ Subject to the current annual cap, California gives rebates amounting to 20 percent of qualifying production costs on a mo-tion picture, and 25 percent for independent films or for TV series that relocate to the state.” — Michael B. Marois and James Nash Detroit Water Board Approves Buying Back $1.47 Billion of Bonds (8/25/2014) The Detroit Board of Water Commissioners unanimously ap-proved a proposed buyback of the city’s water and sewer bonds after reaching deals with enough investors to proceed with a planned debt refinancing this week. Owners of bonds from the Detroit Water and Sewerage Depart-ment agreed to sell back $1.47 billion, or about 28 percent, of the system’s $5.2 billion in outstanding debt, the board’s advisers said Friday. Refinancing the bonds will save $241 million over 26 years, with about $11 million in annual savings for the first 19 years. The plan allowed investors to part with their securities at a known price and protects them against losses in federal court. It will also free up cash for the city and potentially speed its emer-gence what state offers the best value i mbm n the municipal market? <Go> from bankruptcy. The buyback’s success means the Michigan Finance Author-ity is on track to issue bonds next week to replace the old debt. It also plans to issue $150 million in additional bonds to finance improvements to the sewage-disposal system. The deal must still be approved by Detroit Emergency Manager Kevyn Orr and U.S. Bankruptcy Judge Steven Rhodes. Should the refinancing move forward as planned, investors and bond insurers would drop their objections to the water and sewer portions of Detroit’s debt-cutting plan, according to court records. That may shorten the bankruptcy trial and make it easier for the city to win approval of its proposal. The water and sewer bondholders are among the final obstacles to the resolution of the bankruptcy after the city reached agree-ments with general-obligation investors and pensioners during 13 months under court protection. Bondholders had balked at the city’s debt-adjustment plan, which seeks to cut interest rates on some securities or scrap provisions that protect investors from being forced to resell bonds before they mature. The proposal led the three biggest credit rat-ers to lower their grades on the bonds to junk. Once the refinancing is done, any original debt still outstanding will be unaffected by the proceedings. In contrast, about 43 per-cent of the water and sewer bonds would be impaired under the bankruptcy debt-cutting plan, Fitch said in a report last week. — Chris Christoff and Brian Chappatta 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 5. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 5 Texas Notes at 0.13% (8/27/2014) Texas sold $5.4 billion of one-year notes at a record-low yield for the second-most populous U.S. state of 0.13 percent, according to the comptroller’s office. The borrowing, which will pay for schools and other expenses before receiving tax revenue, is the state’s smallest short-term note sale since 2007 and beat last year’s previous all-time low of 0.201 percent. The offering also came in below benchmark one-year yields of 0.15 percent, according to data compiled by Bloomberg. Buyers submitted bids for about $19.6 billion of securities, Comptroller Susan Combs said in a statement. The state has the highest credit grades from the three biggest rating companies. “The competitive bids for today’s sale show that investors are very confident in the Texas economy,’’ Combs said. Texas is home to seven of the 15 fastest-growing cities in the U.S. — Darrell Presston Detroit at 4.85% The Michigan Finance Authority began pricing $1.8 billion of rev-enue bonds on behalf of the Detroit Water and Sewerage Depart-ment to finance the purchase of debt from investors last week. The sale includes a $121 million uninsured senior-lien por-tion maturing in July 2044 that’s being offered at a 4.85 percent yield, according to three people with knowledge of the terms who requested anonymity because the deal isn’t final. The rate is 1.73 percentage points more than benchmark munis, data compiled by Bloomberg show. Detroit won investment grades on its new water and sewer bonds from Standard & Poor’s yesterday, getting a BBB+ rating, the eighth-highest rank. S&P’s rating is the highest among the three biggest credit raters. Moody’s released a report late Monday that rated the senior-lien bonds Ba2 and the second-lien debt Ba3. Those grades are four and five steps lower than S&P’s, respectively. Fitch Ratings as-signed grades of BBB- and BB+, two and three levels lower than S&P’s, respectively. The refinancing is supposed to save $11.4 million a year for the first 19 years of the deal, Nicolette Bateson, chief financial officer for the water and sewer department, said in court Monday. It would also raise $150 million for projects to improve the city’s sewage system. Some bonds are backed by Assured Guaranty Municipal Corp. and National Public Finance Guarantee Corp., according to the people with knowledge of the deal. — Brian Chappatta NEWS SEC Charges Kansas (8/12/2014) The SEC charged Kansas with failing to disclose a “multibillion-dollar’’ pension liability to bond investors. Documents for eight bond offerings in 2009 and 2010 by the state’s Development Finance Authority didn’t tell investors that a study had pegged Kansas’s public-employee pension as the second-most underfunded in the nation. Kansas, which didn’t admit or deny the findings, put in place new disclosure policies and agreed to settle the case. “Kansas failed to adequately disclose its multibillion-dollar pen-sion liability in bond offering documents, leaving investors with an incomplete picture of the state’s finances and its ability to repay the bonds amid competing strains on the state budget,’’ LeeAnn Ghazil Gaunt, chief of the SEC Enforcement Division’s Securities and Public Pension Unit, said in a statement from Washington. The SEC settled a similar case with New Jersey in 2010, the first time the regulator targeted a state. Last year, Illinois became the second state to settle with the SEC over charges it misled inves-tors about a growing shortfall in its employee pension funds as it sold $2.2 billion in bonds. Around the same time as New Jersey’s settlement, the SEC began questioning the disclosures in eight Kansas bond issues that raised $273 million, the SEC said. As the Sunflower State prepared to issue $127 million of bonds in 2009, a draft actuarial report provided to Kansas’s public pen-sion found that the gap between its liabilities and assets had grown to $8.3 billion in 2008, from $5.6 billion the previous year, lowering the pension’s funding level to 59 percent, the SEC said. The gap was the result of years of insufficient contributions by the state and school districts to cover the cost of benefits earned by public employees and their accumulated liabilities, the SEC said. Only Illinois had a lower pension funding status than Kansas. Neither the finance authority nor the Kansas Department of Administration, which advised the authority of material changes to state finances, determined that additional disclosure regarding the pension fund in the bond offering statement was necessary, the SEC said. Kansas has adopted new policies and procedures to ensure it’s making appropriate disclosures about its pension liabilities. The state mandated closer communication and cooperation among agencies responsible for preparing bond disclosures and estab-lished a disclosure committee, the SEC said. The SEC didn’t seek financial penalties or make claims of intentional misconduct, according to Jim Clark, the state’s sec-retary of Administration. — Martin Z. Braun 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 6. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 6 NEWS Perry’s Final Months Leading Texas Clouded by Indictment MARK NIQUETTE (8/18/2014) Texas Democrats are calling for Governor Rick Perry to resign after being indicted yesterday, while Republicans say the charges are politically motivated and won’t stop him from governing or even running for president. Perry, a possible 2016 Republican candidate for the White House who leaves office in January after more than 13 years, faces charges of abusing his powers by vetoing money for pros-ecutors who investigate public corruption. An arraignment date will be set next week, said special prosecutor Michael McCrum. Texas Democratic Party Chairman Gilberto Hinojosa said in a statement that Perry should step down because he “brought dishonor to his office, his family and the state of Texas,’’ even as Republicans and Perry’s lawyer said he was indicted “in a political prosecution’’ for exercising his constitutional authority. Perry, 64, is accused of trying to force Travis County District At-torney Rosemary Lehmberg, a Democrat, to resign by threaten-ing to veto funds for the state’s public integrity unit, which oper-ates from her office and investigates corruption. A Travis County grand jury accused him of abuse of official capacity and coercion of a public servant in the indictment. Perry asked Lehmberg to resign after her arrest for drunken driving last year. David L. Botsford, a criminal defense lawyer representing Perry, said the governor has a legal right and duty to veto spending. The indictment “sets a dangerous precedent by allowing a grand jury to punish the exercise of a lawful and constitutional authority afforded to the Texas governor,’’ he said. McCrum has said there’s evidence to support both counts. Craig McDonald, director of Texans for Public Justice, the non-profit Prepa Gains Extension BRIAN CHAPPATTA (8/15/2014) group that filed a complaint with the district attorney over the governor’s actions, said Perry should weigh resignation. “A governor under felony indictment should consider seriously stepping down,’’ McDonald said. Steve Munisteri, chairman of the Republican Party of Texas, said Democrats calling for resignation are being hypocritical when they made no similar demands of Lehmberg or other Democratic officeholders who got in legal trouble. Perry is facing “the criminalization of what is normal political ac-tivity’’ in the indictment by a grand jury drawn from a Democratic area of the state, he said. “The vast majority of Texans are going to think this is a political prosecution,’’ Munisteri said. The Puerto Rico Electric Power Authority, the main supplier of electricity in the struggling U.S. territory, said it agreed with credi-tors to delay repayment of bank loans until March. The agency uses the lines of credit to buy fuel. It was sched-uled yesterday to repay $146 million to Citigroup Inc. unit Citibank and $525 million to a syndicate of banks led by Scotia-bank de Puerto Rico, which is serving as administrative agent. Prepa, which has $8.6 billion of debt, had already pushed back payments last month after using $41.6 million of reserves to pay investors July 1. Under the agreement, Prepa must appoint a chief restructuring officer by Sept. 8 and come up with a five-year business plan by Dec. 15, according to a statement the utility released yesterday. Prepa must also deliver a debt restructuring plan by March 2. The announcement “is an important milestone in the transfor-mation of Prepa and gives us a clear line of sight to the future,’’ Harry Rodriguez, president of Prepa’s board of directors, said in the statement. The utility said it will make full debt-service payments during the term of the agreements. The agency must repay about $214 mil-lion to bondholders on Jan. 1, according to advisory firm NewOak. Investors have been speculating that Prepa would be the first Puerto Rico public corporation to use the island’s new debt-restructuring law to reduce obligations. Prepa would represent the largest restructuring ever in the muni market, exceeding the $8 billion of GOs and water-and-sewer debt in Detroit’s bankruptcy. Most holders of Prepa debt don’t have insurance. Bond funds affiliated with Franklin Resources Inc. and Oppen-heimer Rochester Funds filed a lawsuit saying the Puerto Rico Public Corporation Debt Enforcement and Recovery Act, ap-proved by lawmakers in June, is unconstitutional. Some of the longest-maturing Prepa bonds have rallied since reaching as low as 34 cents on the dollar July 2. Uninsured Prepa securities due in 2042 traded Aug. 13 at about 50 cents on the dollar, the highest since June 26. That was the day Fitch downgraded the authority to CC, citing a probable restructur-ing or default. Follow Brian Chappatta on Twitter for regular updates and additional insights @bchappatta 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 7. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 7 CREDIT CLOSE-UP (8/28/2014) Pennsylvania Issuers Again Turn to Swaps ‘‘ Last month, commissioners approved an ordinance authorizing a swaption in-volving an upfront payment to the county that Wenger says would go toward debt service. The counterparty, Royal Bank of Canada, would have the right at a future date to compel the county to pay a float-ing rate in exchange for fixed payments until 2033. Transactions involving immediate cash have “been the cause of 99 percent of the abuse in the market,’’ said Lucien Calhoun, the Flourtown, Pennsylvania-based president of Calhoun Baker Inc. The company administers the Delaware Valley Regional Finance Authority, which provides municipal loans. Calhoun said the agency uses swaps for Pennsylvania localities to reduce borrowing costs. Pennsylvania municipalities are turning once again to the kinds of derivative deals that backfired during the credit crunch as the lure of upfront cash and the potential to cut costs prove too hard to resist. Dauphin County in July cleared the way to enter into an interest-rate swap on a deal that helped settle the debt of the formerly insolvent state capital Harrisburg. Berks County, which in 2009 spent about the equivalent of its parks and library budgets to end swaps, agreed to a new contract in March. Lancaster County in November and the Oley Valley School District in 2012 exited deals in exchange for immediate cash and new accords. The governments are tapping swaps even as borrowers pay to end money-los-ing deals. In 2009, Pennsylvania had the most local governments using swaps on variable-rate debt, according to Moody’s. “You’ve got to think long and hard before you take a risk that you have no control over,’’ said Steven Goldfield, who helped develop Harrisburg’s recovery plan as senior counselor at Public Resources Ad-visory Group. “As a governmental official with public funds, you want to preserve the funds.’’ Even after federal regulators pushed through rules sparked by the swaps fallout, public money remains at risk, according to Pennsylvania state sena-tors backing stronger restrictions. Their bills, up for a vote as soon as next month, would have barred the latest deals. “We still have a lot of risky transac-tions that are not working out well for the taxpayers,’’ said state Senator John Eichelberger, a Republican sponsor of the measures. “We need more protection built into the law.’’ In the last eight years, about 1,000 audits of school districts, including those who’ve engaged in swaps, have shown that “whatever benefit they got upfront wasn’t worth it on the back end,’’ said Auditor General Eugene DePasquale. Swaps figured in the fiscal woes of Har-risburg, which was forced into the state’s first receivership in 2011. In response, state senators pushed bills that would limit the use of swaps through steps such as banning upfront payments and mandating that municipalities be able to exit deals at no cost when the contracts are longer than 10 years. Dauphin County backed the incinerator debt and made payments that the city skipped. As part of the settlement that al-lowed Harrisburg to exit receivership, the county contributes a portion of the interest rate on $24 million in fixed-rate bonds that financed the December sale of the waste facility, said Jay Wenger, managing direc-tor at Susquehanna Group Advisors Inc., the county’s financial adviser. Dauphin hasn’t entered into the contract. In 2011, it agreed to two swaps with RBC, effective in 2015 and 2016, that would cost about about $626,000 combined to termi-nate, according to Susquehanna. Wenger said commissioners would do the third swap to manage their interest-rate risk, the same reason for the 2011 deals. “They’ve been very judicious with their evaluation and decision-making,’’ Wenger said. “If you’re using the right tool for the right job, you’re probably going to have a lot of success with that tool.’’ “All proposals are advanced in full compliance with Pennsylvania law,’’ which requires municipalities to use an inde-pendent adviser, Lauren Hopkinson, a spokeswoman for RBC, said in an e-mail. “In each instance, the financial risks and benefits are fully vetted’’ by the adviser, she said. Even though federal law requires independent advisers for municipalities entering into swaps, the compensa-tion the advisers earn through the deal “compromises their independence,” said state Senator Rob Teplitz, a Democrat representing Harrisburg. In Berks County, finance director Robert Patrizio said it was his idea to enter a transaction in March. Berks has returned to the swaps market after the government lost money on ear-lier deals, he said. In 2009, the county paid termination fees totaling $13.8 million, about its budget for libraries and parks that year. The March structure, as with one from 2011, is a basis swap in which the county pays a variable rate based on tax-exempt municipal notes and receives from PNC Bank an amount based on a taxable variable rate, docu-ments show. Patrizio said that for the 2011 transac-tion, he asked the county’s financial advis-er to pull 10 years of historical averages for the two rates and to determine how the county would fare if the contract were in place by each month. The March swap would save at least $2.6 million over its 23-year term; reserves would cover exit payments if needed, Patrizio said. — Romy Varghese You’ve got to think long and hard before you take a risk that you have no control over. ‘‘ 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 8. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 8 CREDIT CLOSE-UP (8/15/2014) Michigan Towns Ready More Pension Bonds Michigan municipalities, facing a year-end deadline to borrow for retirement costs, are planning record bond sales to pay for workers’ health care and pensions. The Detroit suburb of Macomb County plans a $270 million sale, its biggest ever, to finance retiree health-care costs. Kalamazoo is considering a $100 million deal. Bloomfield Hills plans to borrow a record $17 million for pensions. The law allowing the practice expires Dec. 31. States and cities are struggling with how to pay for promises to workers. Yet few communities see debt as the answer — sales of revenue-backed pension bonds have tallied $356 million this year. Interest rates close to five-decade lows are mak-ing it more attractive to pursue the risky strategy of investing borrowed funds. “We can’t afford to wait,’’ said Peter Provenzano, Macomb County finance director. “Timing the market is difficult. You could sit on the sidelines and miss out on an opportunity.’’ Municipalities have sold pension bonds since 1985, led by Illinois and California, according to the Center for Retirement Research at Boston College. This year’s issuers include Orange County and the city of Riverside, both in California. Investing borrowed cash to pay for health expenses is a new twist in Michi-gan, where 284 municipalities owed a combined $12.7 billion in unfunded liabili-ties for retiree medical care, according to Michigan State University. About half didn’t require employee contributions. The practice of issuing debt for retire-ment costs draws criticism from Matt Fabian, managing director at Municipal Market Advisors. The borrowing shows a lack of political will to raise taxes or reduce benefits, he said. From the issuer’s standpoint, the sales’ timing dictates the success of pension bonds, according to the Boston College center. Reinvested proceeds must earn more than it costs to service the debt. Because of stock-market gains follow-ing the recession that ended in 2009, the majority of pension bonds have gener-ated positive returns as of February 2014, according to the center. That’s a reversal for health-care costs, and won’t be able to afford the premiums by the mid-2020s, said Provenzano, the finance director. The bonds will allow the county to keep up with projected cost increases, he said. The plan projects that debt proceeds will earn an average of 7.5 percent annually. “We’re being proactive about this,” Provenzano said. Money from the issue will be invested over the course of a year to adjust to swings in financial markets, he said. With 850,000 residents, Macomb abuts Detroit’s northeast border and is domi-nated by 155 auto plants and suppliers, and the General Motors Technical Center in Warren. The county’s $53,628 median household income compares with about $48,500 statewide. Oakland County, which also borders Detroit, sold $350 million in GOs last year to refinance debt issued in 2007 for retiree medical benefits. Investments from the 2007 issue gained more than projected, result-ing in overfunding for health benefits, said Robert Daddow, county deputy executive. The refinancing will save at least $125 million over the 13-year bond repayment, he said. The county also reduced costs by clos-ing its defined-benefit health plan to new hires in 2006, Daddow said. Kalamazoo may borrow $100 million to partly finance $188 million of retiree health-care liabilities. A city panel this week recommended the bonds and negotiations with retirees and unions to lower medical costs. The city pays $6 million annually from its $50 million general fund toward retiree health care. If investment returns fall short of repay-ing the debt and health insurance, the city would renegotiate with employees for savings, said Tom Skrobola, Kalamazoo finance director. Without revenue from borrowing, the city won’t keep up with ris-ing medical costs and demands for other city services, he said. “We’ve had great success with bargain-ing, but it’s not enough,’’ he said. “It has to be a combined approach.’’ — Chris Christoff from mid-2009, when the financial crisis left most of the deals in the red. The analysis is complicated because many of the securities have 30-year maturities, according to the center. Grand Rapids won’t use debt to finance $135 million in unfunded health-care liabili-ties, said Scott Buhrer, the city’s CFO. ‘‘ We can’t afford to wait. Timing the market is difficult. You could sit on the sidelines and miss out on an opportunity. ‘‘ “The best way to have odds in your favor is to do this when stock prices are de-pressed,’’ Buhrer said. “We’re in the latter stage of a bull market.’’ Michigan didn’t allow such borrowing until a 2012 law, which limits sales to local governments with at least a AA rating, and requires state approval. A bill to extend the law for a year awaits action in the house after passing the senate. Republican Gover-nor Rick Snyder supports the extension. Borrowing for retirement costs works when coupled with benefit changes, said John Axe, a bond attorney based in Grosse Pointe Farms, Michigan. Axe said he represents six municipali-ties that are considering borrowing for the expenses; he declined to name them. Macomb County is paying half the rec-ommended $30 million annual expense 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 9. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 9 CREDIT CLOSE-UP Port St. Lucie, Florida (8/07/2014) ‘‘ We’re done with this type of economic development program. It’s been a ‘‘ traumatic experience. The crowd of 80,000 revelers went wild as a lifelike hologram of rapper Tupac Shakur took the stage at the 2012 Coach-ella Music Festival. Six months later, the Florida visual-effects firm that resurrected the deceased musician in the California desert would itself be dead. Its debt, $37 million owed by taxpayers, lives on. While Digital Domain Media Group filed for bankruptcy nine months after mov-ing into a state-of-the-art studio in Port St. Lucie, Florida, local taxpayers are on the hook for the building’s bonds through 2031. The $3.5 million payment due this year amounts to about 4 percent of Port St. Lucie’s operating budget. “We’re done with this type of economic-development program,’’ said Ed Fry Jr., treasurer of the city of 170,000 about 100 miles north of Miami. “It’s been a trau-matic experience.’’ Florida filed a lawsuit last month alleging fraud by the company. The city council called a meeting last week to consider selling the now-empty studio for as little as $8.5 million. The city tapped its general fund to make last year’s debt-service payment. With another payment due Sept. 1, the city has been trying to convince bondholders to approve a refinancing plan. As of the end of June, investors owning 28 percent of the bonds had agreed to the plan, according to a July 18 city memo. That’s less than the 51 percent threshold required for changing borrowing terms. Studio bonds maturing in 2031 traded Aug. 5 as high as 102 cents on the dollar, compared with about 97 cents when the debt was sold in 2010. They traded most recently at an average yield of about 4.7 percent, or 3.1 percentage points above benchmark debt. S&P grades them A. “The bonds are trading still pretty strong, not at anywhere close to what you would consider a distressed level,’’ said Michael Schroeder, chief investment officer at Wasmer, Schroeder & Co., which man-ages about $3.5 billion in munis. “The market is still believing that the city is on the hook.’’ “Debt-service payments on the Series 2010 Bonds are coming too fast, and too soon,’’ Fry wrote in an April 21 letter to investors. Politicians in Port St. Lucie voted unani-mously in 2009 to build a 115,000-square-foot facility for Digital Domain, after the company received a $20 million grant from Florida on the promise of creating 500 jobs. The city sold $40 million in bonds in 2010. Local officials hailed the studio as a salve for a recession-battered economy built on tourism and construction. Unem-ployment was 13.1 percent when the deal was approved in November 2009, higher than the U.S. rate of 9.9 percent. controlling stake in an indebted California company. That company’s debt weighed down the Florida startup, forcing it to bor-row more to keep the doors open, accord-ing to the suit. Textor got financing from a group of hedge funds at “predatory’’ terms designed to send Digital Domain into a “death spiral,’’ the state’s complaint said. The lenders, led by Tenor Opportunity Master Fund Ltd., took short positions in the stock of Digital Domain, which was running low on cash in the months before it failed. The hedge funds received $35 million from the sale of the bankrupt com-pany, the complaint said. A representative of Tenor, who declined to provide his name when reached by phone, said the company had no com-ment on the lawsuit, in which it isn’t named as a defendant. The complaint describes Digital Domain, which was awarded $135 million in state and local-government subsidies, as a Ponzi scheme. Textor, 48, denies the allegations. He blames the hedge funds for forcing the company into bankruptcy while profiting from declines in its stock. Digital Domain was a legitimate business and the Florida studio helped produce visuals for films including “Rock of Ages,’’ starring Tom Cruise, Textor said. Its failure was the result of bad luck and a few unfortunate financial decisions, he said. “The guys that run Ponzi schemes run away with a lot of money,’’ he said. “I lost everything. I invested more than the state of Florida did and lost it.’’ Textor said he feels remorse for how the company’s failure has burdened the city. That’s why he decided to base his new company, Pulse Evolution Corp., in Port St. Lucie, he said. The digital production firm has hired 50 people. That’s no consolation for Michelle Lee Berger, a city council member who voted for the subsidy in 2009. Last week she lis-tened to proposals from companies seek-ing to buy the taxpayer-financed studio. Offers ranged from $8.5 million to $15 million. The council is considering raising taxes this year. “People who haven’t even moved here yet will be paying for what happened to Digital Domain,’’ Berger said. — Toluse Olorunnipa The visual-effects company, which had worked on such films as “Titanic’’ and “Apollo 13,’’ promised to deliver technology jobs with average annual salaries exceed-ing $64,000. CEO John Textor wowed city council members with plans to build a studio that would produce groundbreaking special effects. Rent payments by the company were supposed to back the bonds. When Digital Domain filed for Chapter 11, it dismissed more than 200 workers and stopped paying rent. The state of Florida filed a lawsuit last month seeking to recoup the $20 million grant it gave to Digital Domain. According to the civil complaint filed in Florida circuit court, Textor and his affiliates defrauded the state by withholding information about the company’s financial challenges. The lawsuit alleges that Textor used the state’s grant money to purchase a 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 10. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 10 CREDIT CLOSE-UP (8/14/2014) Los Angeles Fights Banks Over Swaps The Los Angeles City Council is threat-ening to stop doing business with Bank of New York Mellon Corp. and Dexia SA if they refuse to renegotiate swaps. In a 14-0 vote yesterday, the council asked BNY Mellon and Dexia to return $65 million in what the lawmakers called unfair profits and fees paid since 2008 on debt for sewer work. The companies would also risk losing out on future business under the union-backed measure. A six-year statute of limitations is closing for localities to try to recoup payments to Wall Street on bond deals that went awry in the financial crisis. Municipal borrowers nationwide have paid over $4 billion to banks to end swaps. “We need to hold Wall Street account-able where others have not, and let Wall Street know that we’re too big to ignore,’’ Councilman Paul Koretz said. The time limit is approaching for issuers to try to claw back losses by arguing that banks misled them about the risks of the deals, former Congressman Bradley Miller, an attorney with Grais & Ellsworth LLP, said last month. Wall Street banks pitched the transac-tions as a way to reduce borrowing costs. They unraveled after the financial crisis and the Fed’s policy of holding its bench-mark borrowing rate near zero since 2008 turned many swaps into wrong-way bets. If the banks don’t unwind the agree-ments, according to the motion spon-sored by Koretz and backed by municipal employee unions, Los Angeles should terminate other business with them and exclude the companies from future con-tracts. The vote directs the city attorney to “evaluate potential legal remedies’’ against the banks. Kevin Heine, a BNY Mellon spokes-man in New York, declined to comment. Caroline Junius, a Dexia spokeswoman in Brussels, didn’t immediately respond to e-mail messages seeking comment on the measure. Second only to New York in popula-tion among U.S. cities, Los Angeles Santana told the council yesterday. Santana met with representatives of BNY Mellon and Dexia in June, accord-ing to a memo he wrote that month. Dexia was amenable to renegotiating, though a significant discount was unlikely, Santana wrote. BNY Mellon wouldn’t agree to terminate the deal at no cost. He said he’ll keep exploring options with the banks. The financial crisis drove up interest rates on the wastewater bonds and other city debt, something that officials couldn’t have anticipated when the securities were sold two years earlier, Santana said. “Every financial transaction has risks,’’ Santana said in the memo. “When we an-alyze those risks, it is difficult to compare to what could happen due to changing market conditions.’’ Koretz’s motion asserts that BNY Mellon and Dexia are profiting by a combined $4.8 million a year on the swaps. The city might lose an additional $69 million at current rates if the swaps remain in effect until they expire in 2028, said Koretz. Koretz and fellow Councilman Gil Ce-dillo, both Democrats who served in the state legislature, sponsored the motion at the urging of the labor-backed Fix LA Co-alition. In a report this year, the coalition said Los Angeles pays about $300 million a year in interest and transaction fees while cutting services to save money. Lawmakers’ vote yesterday drew cheers from city employees in the council cham-bers, many wearing stickers from Fix LA that read, “Our Streets, Not Wall Street.’’ Oakland, California, considered severing ties with Goldman Sachs Group Inc. last year over a $14.8 million termination fee for a swaps agreement. The contract remains in effect and the city continues to make debt payments, Karen Boyd, a city spokeswoman, said by e-mail. “Hopefully we’ll bring back a few million bucks,’’ Koretz told union leaders and workers after the vote. It’d be “a huge amount for city services if we can pull this off.’’ — James Nash paid $26.1 million in 2012 to terminate another interest-rate swap with BNY Mel-lon and Dexia. The subject of the council’s vote was part of $151.1 million in swaps associated with a portion of $281 million in wastewa-ter- system revenue bonds. Los Angeles sold $316.8 million in bonds in 2006 to refinance debt issued in 1988 for work on the wastewater system. ‘‘ We need to hold Wall Street accountable where others have not, and let Wall Street know that we’re too big to ignore. ‘‘ The city refinanced the debt again last year, reducing the amount by half. Because of a decline in interest rates since 2006, the swaps had a negative fair value of $24.7 million as of June 2013. Ex-iting the contracts would cost from $23.5 million to $25.7 million in termination fees, according to a June analysis by the Public Resources Advisory Group for Miguel Santana, the city administrative officer. Santana advised the council against terminating the swaps in a May memo, saying the financing had saved the city about $21.7 million. “Even today, the swaps are the most cost-effective action when you look back,’’ MONITOR, GRAPH AND ANALYZE GLOBAL CDS MARKETS CDX<GO> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 11. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 11 S&P Widens Lead over Moody’s on Rated Muni Debt (8/12/2014) The chart on the right shows the mar- Moody’s and S&P’s Market Share ket share of long-term fixed-rate muni debt that carried a rating from Standard & Poor’s and Moody’s. Based on the number of deals since 2008, S&P has rated an average of 58 percent of muni deals compared to 48 percent of deals that carried a grade from Moody’s, data compiled by Bloomberg show. In July 2014, 63 percent of deals carried an S&P grade and 44 percent held a rating from Moody’s. Based on par value of deals (not shown in the chart), Standard & Poor’s has a market share of 86 percent on aver-age since 2008; Moody’s, 80 percent. This July, about 86 percent of deals based on par value carried an S&P grade, while 74 percent used Moody’s. — Taylor Riggs DATA 75% 70% 65% 60% 55% 50% 45% 40% 35% S&P Rated Moody's Rated Jan-2008 Jan-2009 Jan-2010 Jan-2011 Jan-2012 Jan-2013 Jan-2014 Source: Bloomberg Texas Sells Debt at Fastest Pace in Five Years, Bucking Austerity Trend (8/28/2014) Texas is selling debt at its fastest pace Texas Bond Issuance since 2009, issuing $23.4 billion year to date. A surge in issuance from the second-most populous state comes as total issuance in the municipal market is at its lowest since 2011. Total Texas issu-ance for the year through August is above 2013’s $23 billion and 2012’s $20.9 billion. Texas sold $13.9 billion of debt in 2011 and $19.7 billion in 2010. The increase in debt from Texas isn’t hampering demand. This week, Texas sold $5.4 billion of one-year notes at a record-low yield of 0.13 percent, breaking its previous record low of 0.201 percent when it sold debt last year. Bloomberg’s AAA muni benchmark one-year note yields 0.15 percent. — Taylor Riggs 40 35 30 25 20 15 10 5 0 2014 2013 2012 2011 2010 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec In Billions of U.S. Source: Bloomberg FOLLOW TAYLOR RIGGS ON TWITTER>>> FOR REGULAR UPDATES AND ADDITIONAL INSIGHTS @TaylorRiggsMuni 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 12. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 12 DATA Sponsored by Pittsburgh Shakes Off Recession, Population Drop TAYLOR RIGGS (8/22/2014) Pittsburgh’s population and real estate taxes have declined in recent years, but its per capita income topped $50,000 in 2012, above the national average of $43,700. 1. Pittsburgh Population Declines 2. Real Estate Taxes Fall Below Budget 3. But Expenditures Keep Pace With Revenues 4. And Per Capita Income Above National Levels 5. Debt Service Falls as Pension Costs Increase 6. Pittsburgh Sells Wrapped Debt With Tighter Spreads $55,000 $50,000 $45,000 $40,000 $35,000 Pittsburgh Per Capita Income U.S. Per Capita Income PA Per Capita Income http://briefs.blpprofessional.com/viz/Pittsburgh-Shakes-Off-Recession-Population-Drop/index.html E-mail questions or comments on Bloomberg Brief StoryCharts to Deirdre Fretz at dfretz@bloomberg.net CLICK HERE TO LAUNCH the StoryChart in your internet browser. $30,000 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Source: Pittsburgh POS Worst City Pension Plans in Michigan, 2013 (8/19/2014) POSITION CITY FUNDED RATIO TOTAL POPULATION* TOTAL PENSION UNFUNDED ACCRUED LIABILITIES ($MILLIONS)** UNFUNDED PENSION LIABILITY PER CAPITA ($) 1 Bloomfield Hills 50.7 3,882 15.032 3,872 2 Flint 61.1 100,515 322.876 3,212 3 River Rouge 58.9 7,951 24.686 3,105 4 Norway 50.6 2,864 8.597 3,002 5 Saginaw 55.4 51,776 145.679 2,814 6 Traverse City 64.9 14,702 34.173 2,324 7 Ecorse 48.1 9,545 21.973 2,302 8 Hamtramck 54.2 22,317 45.508 2,039 9 Melvindale 52.3 10,637 21.649 2,035 10 Lansing 66.9 113,488 218.261 1,923 11 Manistique 51.7 3,102 5.936 1,914 12 Crystal Falls 66.2 1,540 2.835 1,841 13 Lincoln Park 32.0 37,998 69.115 1,819 14 Escanaba 64.0 12,609 21.979 1,743 15 Huntington Woods 52.7 6,236 10.814 1,734 16 Iron Mountain 51.0 7,662 13.147 1,716 17 Wayne 70.8 17,562 29.229 1,664 18 Fraser 50.8 14,563 23.960 1,645 19 Jackson 55.3 33,661 54.620 1,623 20 Highland Park 47.0 11,971 18.728 1,564 State of Michigan 61.3 9,883,360 31,199.500 3,157 * Most recent population data available from Census **Does not include OPEBs 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 13. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 13 DATA Sponsored by Yale Reputation Can’t Bail Out New Haven TAYLOR RIGGS (8/15/2014) Moody’s rated New Haven’s GOs A3 due to “an extremely narrow financial position resulting from several years of structurally imbalanced operations.” 510 500 490 480 470 460 In Millions of U.S. Dollars Tale of Two States TAYLOR RIGGS (8/08/2014) Wisconsin’s 10-year yield trades at 2.60 percent, below Connecticut’s 2.65 percent. In April 2013, Wisconsin’s 10-year yielded 2.48 percent compared with Con-necticut’s 2.40 percent. 1. Connecticut GDP Tops Wisconsin 2. Connecticut, Wisconsin Personal Income Rebounds 3. Wisconsin Unemployment Rate Falls 4. Wisconsin 10-Year Yields Lower Than Connecticut 5. Wisconsin Benefits in Pricing With Tighter Spreads 3.6% 3.4% 3.2% 3.0% 2.8% 2.6% 2.4% 2.2% WI 10-Year Yields CT 10-Year Yields Revenues Expenditures http://bit.ly/1kpgyPj E-mail questions or comments on Bloomberg Brief StoryCharts to Deirdre Fretz at dfretz@bloomberg.net CLICK HERE TO LAUNCH the StoryChart in your internet browser. 2.0% Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14 Jul-14 Source: Bloomberg 1. City Budget Structurally Imbalanced 2. Pensions Take Bigger Bite of Budget 3. New Haven Unemployment Tops National Level 4. Yale Acceptance Rate Declines and Endowment Grows 5. Yale’s Net Assets Grow 6. Even With Insurance, New Haven Pays Extra to Borrow http://bit.ly/1uoAsw1 E-mail questions or comments on Bloomberg Brief StoryCharts to Deirdre Fretz at dfretz@bloomberg.net CLICK HERE TO LAUNCH the StoryChart in your internet browser. 450 2010 2011 2012 2013 2014 2015 Source: New Haven City Budget/POS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 14. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 14 Puerto Rico Electric Power Bonds Rebound From July Low TAYLOR RIGGS (8/04/2014) Puerto Rico Electric Power Authority Puerto Rico Electric Power Authority 5 Percent of 2042 bonds were downgraded July 31 to CCC from B- by Standard & Poors, its fourth downgrade in 2014. The bonds were investment grade, rated BBB-, as recently as June of this year. Moody’s downgraded the bonds three times in 2014, most recently to Caa2 on July 1 from Ba3 on June 26. Fitch downgraded Prepa three times this year, from BB+ in February to CC on June 26. Prices fell to a low of $37 on July 1 and have since rebounded to $48.63 last Thursday. — Taylor Riggs DATA 110 100 90 80 70 60 50 40 30 July 1: Fitch downgrades to BBB-Feb June 11: Fitch downgrades to BB; June 18: S&P downgrades to BBB-; June 26: Fitch downgrades to CC; June 27: S&P downgrades to BB 18: Fitch downgrades to BB+ July 9: S&P downgrades to B-; July 31: downgrades to CCC June 19: Moody's downgrades to Baa3; June 20: S&P to BBB Aug 26: Barron's article in August on PR Feb. 7: Moody's downgrades to Ba2 June 26: Moody's downgrades to Ba3; July 1: downgrades to Caa2 May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14 Jul-14 Source: Bloomberg Top 14 Cities by Population and Their Pension Plans (8/06/2014) CITY ISSUER FISCAL YEAR TOTAL POPULATION UNFUNDED ACTUARIAL ACCRUED LIABILITIES ($MILLIONS) FUNDED RATIO UNFUNDED LIABILITIES PER CAPITA ($) City of New York, NY 2013 8,336,697 71,949 60.7 8,630 City of Los Angeles, CA 2013 3,857,786 9,769 77.1 2,532 City of Chicago, IL 2013 2,714,844 20,110 34.3 7,407 City of Houston, TX 2013 2,161,686 2,971 76.2 1,374 City of Philadelphia, PA 2013 1,547,607 5,461 47.4 3,529 City of Phoenix, AZ 2013 1,488,759 2,538 60.9 1,705 City of San Antonio, TX 2013 1,383,194 313 91.9 227 City of San Diego, CA 2013 1,338,354 2,279 68.6 1,703 City of Dallas, TX 2013 1,241,108 1,750 79.2 1,410 City of San Jose, CA 2013 982,783 1,772 71.6 1,803 City of Austin, TX 2013 842,595 1,463 68.0 1,737 City of Jacksonville, FL 2013 836,507 2,706 51.4 3,235 City of Indianapolis, IN 2013 835,806 816 7.9 976 City & County of San Francisco, CA 2013 825,863 3,414 83.1 4,134 * Population from Census 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 15. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 15 DATA Popular Municipal Securities on Bloomberg August 26, 2014 (published 08/27/2014) MSRB MARKET FLOW (08/29/2014) Top Traded Borrowers in the Municipal Market 8/22/14 to 8/28/14 ($millions) DEALER TO CLIENT VOLUME DEALER TO DEALER ISSUE BORROWER** VOLUME CUSTOMER SELLS CUSTOMER BUYS NET VOLUME Total 24742 5375 10933 -5558 8434 1 Michigan Finance Authority 1386 24 1287 -1263 74 2 State of California 686 194 233 -39 259 3 State of Texas 515 45 448 -403 21 4 City of New York NY 506 112 162 -50 232 5 University of Colorado 328 14 296 -282 17 6 New York State Dormitory Authority 260 71 89 -18 101 7 State of Washington 255 53 66 -12 137 8 New York City Water & Sewer System 247 78 85 -7 85 9 State of Maryland 231 47 73 -26 111 10 Alabaster Board of Education 219 28 95 -67 96 Source: Bloomberg * excludes variable rate & derivative debt *“Borrower” is defined as a municipality, an enterprise fund of a municipality or 3rd party obligor * Volume numbers treat trades > $5MM as $5MM due to MSRB reporting restrictions MFLO<GO> POPULARITY DESCRIPTION STATE COUPON MATURITY AMOUNT OUTSTANDING ($MILLIONS) BLOOMBERG MARKET SECTOR CALL PROVISIONS DATED DATE FEDERAL TAX 1 Puerto Rico-A PR 8.000 07/01/35 3500 General Obligation Call/Sink 03/17/14 Exempt 2 IL St Txb-Pension IL 5.100 06/01/33 7650 General Obligation Sinkable 06/12/03 Taxable 3 PR S/Tax-Cabs-A PR 0 08/01/54 7620 Sales Tax Sink/MW Call 07/31/07 Exempt 4 Liberty Dev Goldman NY 5.250 10/01/35 1243 Economic Development MW Callable 10/12/05 Exempt 5 PR-Ref-A PR 5.000 07/01/41 633 General Obligation Call/Sink 04/03/12 Exempt 6 PR Aqueduct-A-Sr Lien PR 5.250 07/01/42 551 Water/Sewer Call/Sink 02/29/12 Exempt 7 PR Elec Pwr-A PR 5.000 07/01/42 358 Public Power Call/Sink 05/01/12 Exempt 8 PR Elec Pwr-Xx PR 5.250 07/01/40 588 Public Power Call/Sink 04/07/10 Exempt 9 Bay Area Toll Auth-B CA 1.500 04/01/47 552 Toll Highways/Bridges/Tunnels Call/Put/Sink 08/05/14 Exempt 10 ID Hlth Fac Auth-A ID 4.125 03/01/37 36 Hospital Call/Sink 08/20/14 Exempt 11 Salt Verde Fnl Corp AZ 5.000 12/01/37 565 Gas Forward Contract Sink/MW Call 10/25/07 Exempt 12 PR-Ref-A PR 5.000 07/01/35 323 General Obligation Call/Sink 04/03/12 Exempt 13 FL Hurricane-Ser A FL 2.995 07/01/20 1000 Miscellaneous MW Callable 04/23/13 Taxable 14 Texas Transprtn-A-Ref TX 5.000 08/15/41 462 Toll Highways/Bridges/Tunnels Call/Sink 11/01/12 Exempt 15 CA Cmnty Dev Auth-A CA 5.000 04/01/42 870 Hospital Callable 04/18/12 Exempt Source: Bloomberg SECF<GO> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

- 16. 09.11.14 www.bloombergbriefs.com Bloomberg Brief | Municipal Market 16 “FIRST-LOSS” REINSURANCE PROTECTION IS BUILT IN, SO WE CAN PROTECT OUR CAPITAL AND YOURS. Bond insurance isn’t a commodity anymore — Build America Mutual’s unique characteristics set us apart. Visit buildamerica.com/mission to learn what else makes us diff erent, including: • BAM’s mutual structure, which means a stronger balance sheet and durable ratings • Low-risk, municipal only underwriting with no exposure to structured fi nance or Puerto Rico • Obligor Disclosure Briefs — free, annual updates on every credit we insure • Unique economic benefi ts for issuers © 2014 Build America Mutual sponsored by 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16